Following the Police Federation Conference there was a lot of media interest in the colleague who stated that her accountant had suggested she quit, work 22 hours a week and claim benefits because she couldn’t live on £40,000 a year. Of course, I don’t know her personal circumstances, but my first thought was – what the h377 is she spending her money on? I never earned that much and was the sole earner for a household of six, but I never (a) screamed poverty (even though I frequently screamed ‘skint’), and (b) could never have afforded an accountant. As I said, though, I do not know her circumstances and as such my knee-jerk response was a bit focused on my experience and not those of serving colleagues.

But.

While the cost of living has certainly rocketed of late, I’m not sure the Retail Price Index takes into account the Starbucks that people take for a drive/walk on the way to and from work, the factoring-in of the price of the less-than-five-year-old cars I see as normal in a police car park, nor the cost of an armful of tattoos – which my brief research suggests is easily £1,000 an armful (£700 for an 8×8 pic).

All of this research and personal experience underlined the fact(?) that people are not taught, in school, how to manage their income. This was a point also raised and mis-reported by MP Lee Anderson recently, where he suggested people were not taught that, nor how to cook. I know I never was, and nor were my children. Life lessons? In school? Heaven forfend, they need to know Welsh and Spanish!

So here is my advice, which I never took because I, too, liked ‘things’ unless and until I couldn’t afford them. But I learned this ugly truth.

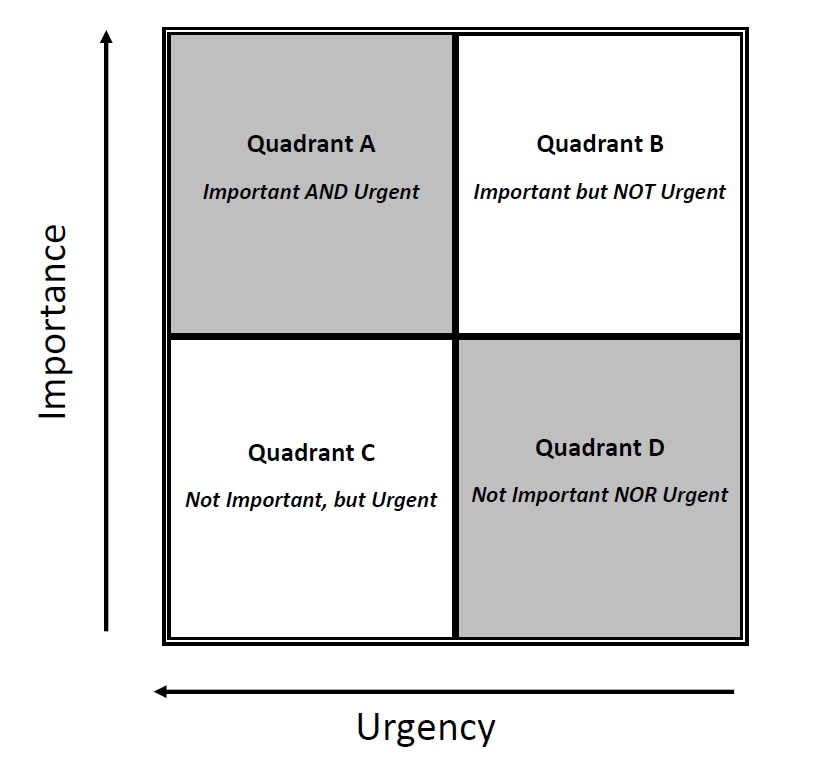

There is a time management tool called the Time Matrix. It is divided into four quadrants, where how your time is used is identified by two criteria, Importance and Urgency. It looks like this.

I’ll not insult you by explaining it, although that can be done by reading my book Police Time Management, but as you can see, tasks in each quadrant are identified as (for example) Urgent AND Important, Urgent NOT Important, Important NOT Urgent, and neither.

Now consider your spending habits. What have you bought, recently? Where did that purchase sit? I recognise there are some value judgements to be made, here, but I would respectfully argue that some of the aforementioned purchases (e.g. a new or leased car as opposed to cheaper, paid for older model; tattoos; the latest iPhone; Starbucks other-expensive-luxury-coffee-brands-are-available drinks; nights on the lash) RARELY EVER hit the top half of the Matrix.

If you are struggling, you really have to decide for yourself where economies can be made – and your ego and feeling that self-worth is dictated by what other people think of your car/address/body art/coffee choice should be utterly ignored when making those decisions. Leasing a new car is great, except at the end of the lease period you don’t own a car that is an asset you can sell. Duh!

Until I retired and got my lump sum the average age of my car, by choice AND imposition, was 10-15 years. I got bank loans to pay for a 2k and (even) an £800 purchase of cars, when one car was all we could afford. When we needed two, they were also old. Even now, my mum’s estate paid for my (then) 5-year-old sports estate which I will run until it dies. (Which may be a while as it’s still only done 60,000 miles.) Of course, if I win a lottery, I may go nuts. But not until then. And I never left the UK between 1985 and 2015.

How about a mortgage? If you’re renting, find a house that the same monthly amount will buy (but wait until interest rates shrink). Read and listen to Martin Lewis moneysavingexpert.com stuff. But above all, don’t moan about the cost of living when you’re sitting on something that really was purchased from Quadrant D.

I’m sorry if these suggestions hurt your feelings. You earn money to spend it as you want, in a perfect world. But the facts don’t care about your feelings, and you know in your heart that blunt as I am, what I’ve suggested is common sense.

Think hard. It may not solve your problems in a week, but a new approach to spending will make life a little bit easier over time.